FinTech and Financial Service institutions talk a lot about consumer orientation. But if you look at their actual behavior they mainly approach this with an internal perspective and with a focus on innovation in the enterprise, industry or branch. They look what they did before and what they could do better within their existing organization. The most common innovation is to build mobile applications for their sales channel. Without any doubt, this is important for continuous improvement of financial services! But is this disruptive (“blue ocean”) and really customer focused? No, it is not.

What, if these new and old players in financial services were really to take the customers view, and ask themselves what they could do better to solve their customers’ tasks, provide new benefits and ease customer pains[1] ? What if they could be really to open innovation with their just customers like the many successful e-business veterans before?[2]

“Make security a lifestyle decision” is an example of a big change in thinking about what needs innovation and what is, on the other hand a cultural aspect, which should stay unchanged in its manner or meaning. The very difficult and exhausting tasks of security and compliance in digital finance processes, business models and solutions could switch FinTech offerings to provide a unique selling point. Changing security and transparency to become a life style is much more than just speed, necessity and corporate demand. I recommend looking at Thomas Langford’s session at the EIC 2016 “Making Security the Competitive Advantage for your Enterprise”[3].

What if it would be hip to spend money while being protected from double charging. What if transparency as a mind set and self-concept of a business would provide the arguments for blockchain enabled FinTech solution? What if the deep trust, that can be gained by a financial process and its transactions by being stored in a blockchain and the ability to be traced later on became chic and not just useful. This might create new customer and business awareness in handling financial processes and mitigate their related risks.

But to return to a more external view of innovation; as a FinTech you have to change the tools for discovery:

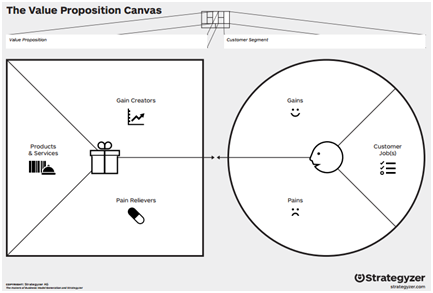

- Take the value proposition canvas[4] for deeper analysis of customer demand of each customer segment and explore where security is a gain or a pain point.

Pic. 1: Value Proposition, Strategizer

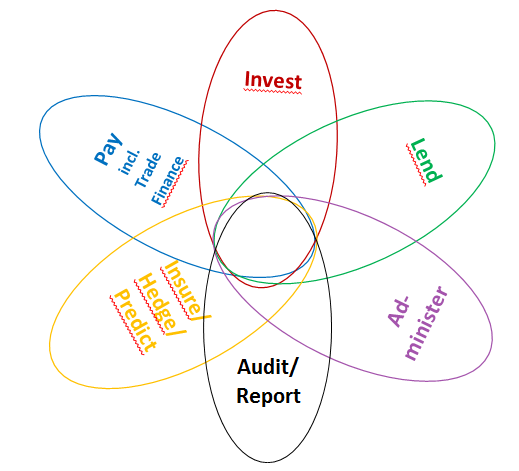

- Take the view of the business demand driven classifications in the “FinTech-Flower” to map the existing finance process solutions in enterprises with digital security offerings:

Pic. 2 FinTech Flower, Gräslund & DeBergami 04/2016

The “FinTech-Flower” (Gräslund & DeBergami 2016) differentiates the following FinTech value propositions:

- INVEST: enterprises invest to increase capital expect variable profit sharing or fixed rates of debt retirement with interest. FinTechs might provide investment or financing projects for external earnings of the enterprise and look for the secure environment, being paid per service.

- LEND: enterprises lend money to finance their working capital or investment. FinTechs might act as agent for third parties and earn percentages of the budget lent, securing trust between the lending partners.

- PAY: enterprises pay their partners and get paid in the value chain. Partial payments and credit vouchers or tax may be part of the payment process. FinTechs might place new crowd and third party partners and replaces banks as former agent for this process get payed by transaction fees.

- ADMINISTER: enterprises obtain assets like shares, raw materials as well as real estate or art. For all these asset management processes, the outsourcing to a Fintech is worth considering, because in these very specialized markets the Fintechs have the deeper market knowledge than the enterprise without high-volume business, as well as to reduce the risk of errors, earning percentages of the administered value and replace former third party providers.

- HEDGE / (IN)SURE / MITIGATE: enterprises secure / insure their asset classes often using insurances or hedge transactions to mitigate their risk. So PREDICTion is a natural part of many of these mitigation processes. FinTechs can act as agents to offer some sort of insurances, rate the creditworthiness of third party providers and provide anti-money laundering security for fixed fees.

- AUDIT & RISK MANAGEMENT: enterprises are legally required to report on their business success and to test their value chain for risk and for technical, economical or legal fraud using three lines of defense. FinTechs could provide help and guidance using the very specialized processes of data science, complex statistics in these investigations if they offer technological support like blockchain solutions or knowledge of analytics an artificial intelligence.

Stay tuned.

[1] See also upcoming research results for the “Fintech-Flower”. Please contact me: [email protected]

[2] http://www.simplyseven.net/

[3] https://www.youtube.com/watch?v=hsq7zgc9C48

[4] http://www.businessmodelgeneration.com/canvas/vpc

{kind=link}